Frequently Asked Questions

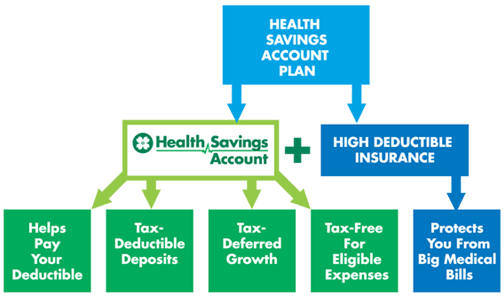

Your Health Savings Account (HSA) coupled with a High Deductible Health Plan (HDHP) can help you save money on your medical expenses. By choosing the HSA Plan you can save significantly on your health care premiums.

General Information

A Health Savings Account (HSA) is an individually owned, tax-advantaged bank account that allows you to accumulate funds to pay for qualified health care expenses. To qualify, you must be covered under a qualified high-deductible health plan (HDHP) as defined by IRS regulations. The State Health Plan Savings Plan is a high-deductible health plan. You can contribute to your HSA through pretax payroll deductions.

You can pay for current qualified health care expenses or save the funds for retirement health care expenses. You are responsible for monitoring your account, including ensuring distributions are for qualified expenses and contributions do not exceed limits set by the IRS. You must keep records and documentation of all health care expenses for which distributions are taken.

HSAs offer a triple tax advantage:

- Contributions are 100 percent tax-deductible for the account holder.

- Funds grow on a tax-deferred basis, and funds are not taxed if used for an eligible expense.

- Funds can be used tax-free for eligible health care expenses.

As you make contributions to your HSA, you can save the funds or spend the funds on current health care expenses. Unused funds and interest carry forward, without limit, from year to year. As the account holder, you own the account and can keep the account even if you change jobs or stop working.

To qualify for an HSA, you must meet the following requirements:

- You must be covered by the Savings Plan, which is a qualified high-deductible health plan (HDHP).

- You must have no other health coverage, including a spouse’s plan that provides benefits covered by your HDHP. You can, however, have accidental, disability, dental, vision or long-term care coverage or coverage that provides benefits for a specific disease or illness, a fixed amount for hospital stays or liability coverage, such as workers’ compensation.

- You are not enrolled in Medicare.

- You do not receive health benefits under TRICARE.

- You have not received Veterans Administration (VA) benefits within the past three months.

- You cannot be claimed as a dependent on someone else’s tax return.

A Limited-use MSA is a Health Savings Account (HSA)-compatible MSA. The Limited-use MSA allows you to set aside money pretax to pay for dental and vision care expenses. If you are enrolled in the Savings Plan, you are eligible to participate in a Limited-use MSA, which will help maximize your tax savings. The HSA can be used to pay all types of medical expenses incurred now or in the future; however, the Limited-use MSA can be used only to pay for current year dental and vision expenses.

Here's a tip. Plan carefully to preserve the value of both accounts by using your HSA funds to save and invest for future health care expenses, or large, unexpected expenses. Use your Limited-use MSA to pay for routine dental and vision care expenses you incur each year.

Enrollment and Contributions

When you enroll in the Savings Plan and elect to make contributions to an HSA, PEBA will notify HSA Central to setup a bank account for you. You will receive a welcome email with directions to activate your account. You will receive your HSA Central debit card within 7 to 10 business days. Be sure to log in to your account online to accept the account's terms and conditions and call to activate your debit card to fully access your new HSA.

To designate a beneficiary, log in to the HSA Central Consumer Portal, select Accounts, then Profile Summary and Add Beneficiary. It's important to review your beneficiary designations periodically to ensure they are up to date.

| 2026 Limit | 2027 Limit | |

|---|---|---|

| Self-only coverage | $4,400 | $4,500 |

| Family coverage | $8,750 | $9,000 |

| Catch-up contribution (ages 55-65) | $1,000 | $1,000 |

Distributions from your HSA

Yes. As long as the qualified health care expense occurred after you opened the HSA, you can pay for the expense or reimburse yourself with HSA funds. Keep copies of your itemized receipts and insurance plan explanation of benefits (EOBs) to verify your funds were used for qualified health care expenses, not paid for by another source or taken as an itemized deduction for a prior tax year.

Qualified expenses are defined by the IRS as amounts paid for the diagnosis, cure, mitigation, treatment or prevention of disease or for the purpose of affecting a structure or function of the body, as well as for transportation primarily for and essential to such care. Qualified expenses generally do not include insurance premiums, but do include premiums for long-term care insurance, COBRA coverage, health care coverage while receiving unemployment compensation, or Medicare and other health care coverage if you were age 65 or older (other than premiums for a Medigap policy, such as the Medicare Supplemental Plan).

See IRS Publication 502 and IRS Publication 969 for more information.

HSA funds can be spent on current year expenses or saved for future expenses to pay for qualified medical, dental, vision and prescription drug expenses as defined in IRS Publication 502. Funds used for non-health care expenses are subject to income tax and, if you are younger than age 65, are subject to a 20 percent IRS penalty.

For a list of qualifying expenses, visit www.irs.gov.

Yes. Individual account holders must file IRS Form 8889 with their annual tax return to report contributions and distributions from the account. HSA Central, will provide two tax forms:

- Form 5498-SA to report the contributions and rollovers made during the previous calendar year; and

- Form 1099-SA to report the total amount of distributions from the HSA.

More Information

Visit the HSA Central website at schsa.centralbank.net or call 833.571.0503. Log in and access your account for:

- Statements and activity;

- Bill Pay services;

- Setting up recurring provider payments; and

- Online investments.